Vehicle valuation is much more than a technical step in the financing process for banks, leasing companies, insurers and other financial institutions. Decisions about financing amounts, the relationship between the value of the vehicle and the loan, insurance, residual value, claims handling, remarketing and portfolio risk management are all based on the estimated value of a vehicle.

That is why the question of data is becoming increasingly important. Which data source do we use? How often is it updated? Does the estimated value reflect the real market situation? And most importantly: what happens if the entire process depends on a single source?

Vehicle valuation today requires more than just a reference value. It also requires a broader market context. In a B2B environment, this means access to high-quality vehicle valuation data, up-to-date used car market data, reliable vehicle pricing data and an independent source that allows organisations to verify whether an estimated value is aligned with the real market.

Relying on one source creates risk

Dependence on a single data source creates several types of risk.

The first is operational risk. If access to data is unavailable, if integrations are limited or if the process temporarily slows down, this can affect financing approvals, internal controls, insurance processes and the daily work of sales or risk teams.

The second is data risk. Even when the source is available, the question remains whether the value accurately reflects the current market situation. This is especially important in segments where prices change quickly: electric vehicles, higher-priced SUVs, imported vehicles, younger used cars or vehicles with specific equipment.

The third is market risk. A bank, leasing company or insurer does not only need the value of an individual vehicle. It also needs to understand the segment. What is happening with the prices of comparable vehicles? Is inventory increasing? Is a certain type of vehicle selling more slowly? Is the local market diverging from the broader European market?

If an organisation does not have an alternative source of market data or an independent source for vehicle valuation, it is difficult to answer these questions in time.

Verification is essential

For banks, the value of a vehicle is linked to collateral and the relationship between the financing amount and the value of the asset. If a vehicle is overvalued, financing risk can increase. If it is undervalued, the bank may limit financing more than necessary.

For leasing companies, the question is even more complex because it is not only the current value that matters, but also the future value of the vehicle at the end of the contract. This is where high-quality residual value data becomes essential, because mistakes in residual value estimation often only become visible years later, when the vehicle returns from leasing and needs to be sold or included in remarketing.

All these institutions have one thing in common: they need the ability to verify. Not because the existing source is necessarily bad, but because a single source cannot always show the full picture.

We can see the same example in the automotive market

The same logic is very clear in the automotive market. Banks, leasing companies, insurers, dealers and other organisations often rely on one main data source for vehicle valuation. Such a source can play an important role in the process, as it enables standardisation, comparability and fast decision-making.

But if the entire process is based on only one source, risk appears. The organisation does not always have the ability to check whether the estimated value reflects the real market situation, whether certain segments are moving faster than expected, or whether comparable vehicles are actually reaching the same prices in the current supply.

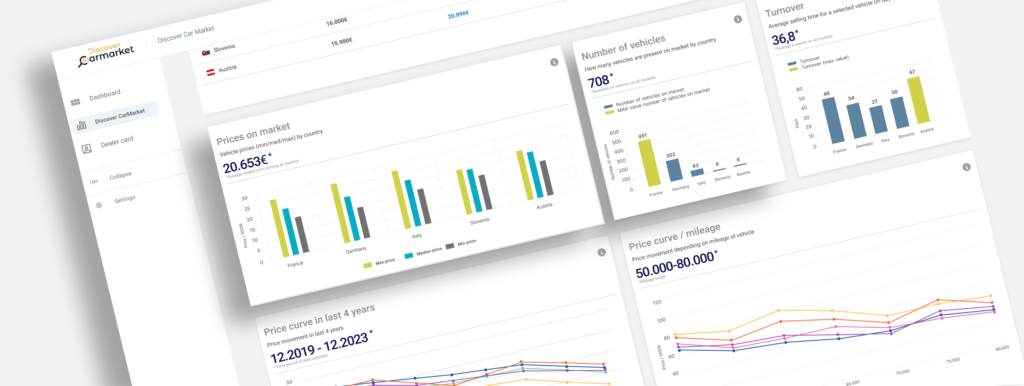

This is especially important in the used car market, where conditions change quickly. This is where Discover Car Market, or DCM, comes in.

DCM is designed as an independent view of the used car market and as a solution for organisations that need broader context when valuing vehicles. It does not offer the user just one additional number. It provides a wider market context: which comparable vehicles are currently available, at what prices they are advertised, how prices differ between markets and whether the estimated value differs from the real market supply.

That is why DCM is an alternative to Eurotax for organisations that do not want to depend on a single data source, or for those that experienced a shock when Eurotax faced problems. At the same time, it can also act as an additional or unique independent source for checking values alongside existing valuation systems.

For banks, leasing companies and insurers, this means greater data resilience. DCM enables financial institutions to check:

- whether the estimated vehicle value is aligned with the real market supply,

- how comparable vehicles are advertised on the market,

- whether there are significant price deviations,

- how individual segments are moving in terms of price,

- whether the local market differs from the broader European market.

In practice, DCM works as a direct source of market truth. It helps reduce dependence on a single system, improve risk control and support decisions based on a broader picture.